As the client had been using this method of disbursement from the company for several years, there was a concern that the tax office would start auditing other tax years. This could lead to liquidation consequences.

And that’s why we had to start looking at Plan B and Plan C from a legal point of view, which were:

➡️ Ensure the continuation of the business; and

➡️ Do not expose the statutory/corporate officers to criminal and commercial risks (unfair liquidation, non-compete, creditor detriment,…)

But the sequel was as follows:

➡️Protokol against the client;

➡️Rozhodnutie FR against the client;

➡️Rozhodnutie FR in favour of the client; and

➡️Rozhodnutie FR in favour of the client.

The discomfort lasted a year and a half with a happy ending (even without a trial).

Attention 👉 : Invoicing to your own company is a red flag for the tax authorities. The reason we won, apart from some luck, was that:

➡️ We have modified the contracts; and

➡️ The tax office was somewhat “led” into an argumentative trap in the audit, which we have exploited in the appeal;

Such payouts are a Slovak evergreen like the shvarc system. And I am happy to lecture on this topic as it is an intersection of legal, tax and levy advice and a defining example of so-called pragmatic structures (i.e. assertive structures in accordance with the law as a response to a less favourable business environment).

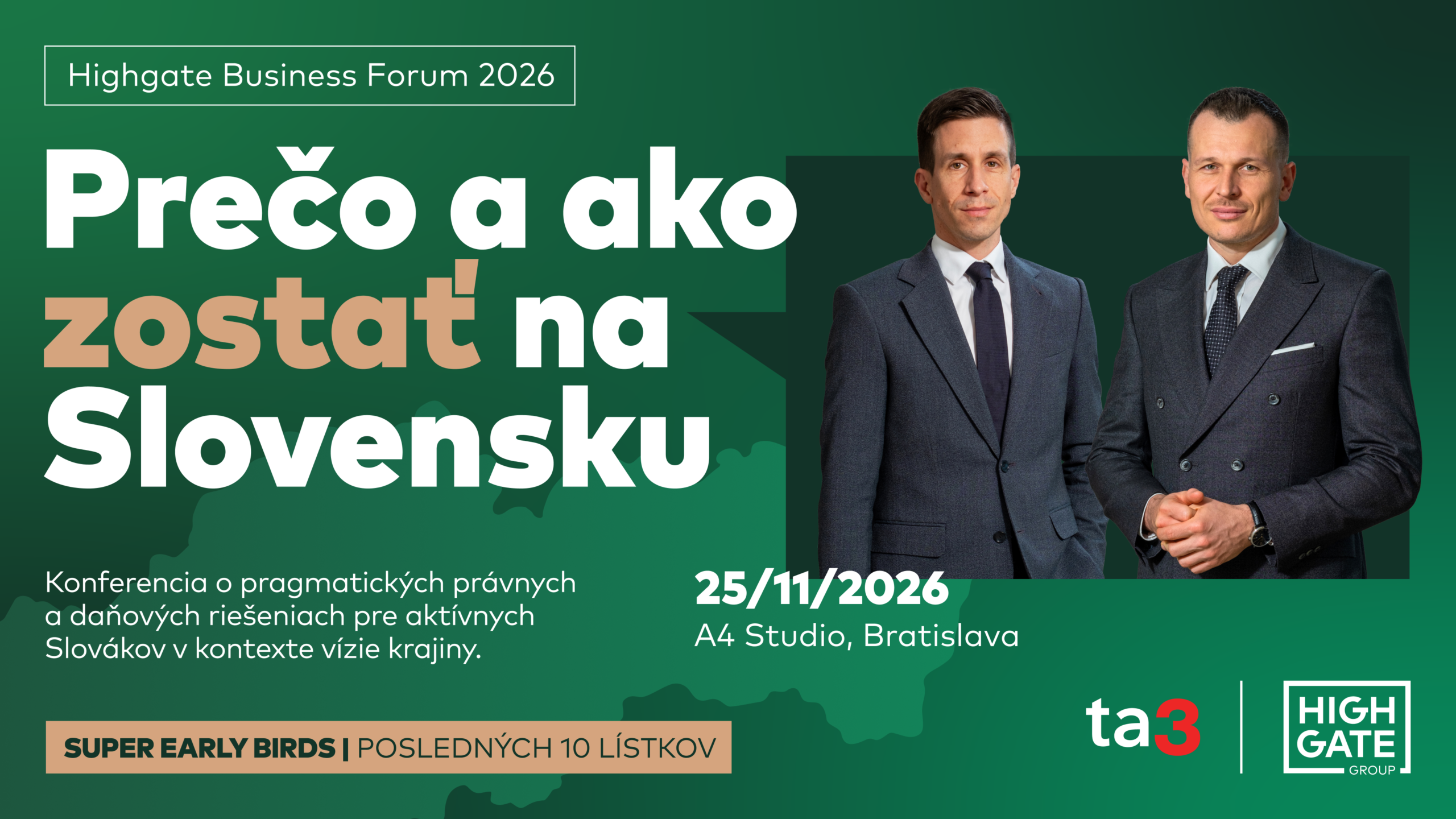

If you are interested in such topics, I would like to draw your attention to two events we organise at Highgate Law & Tax:

🔹Brunch: Czech Republic vs Slovakia in terms of investment taxation together with Patrik Koželuha and Barbora Paclíková – 24.2. at Nivy Tower (link in the 1st comment);

🔹Big conference for entrepreneurs with a fitting name: Why (how) to stay in Slovakia? (link in 2nd comment).