These forms are used to provide an indicative comparison of the net income for 2026 of a self-employed entrepreneur (e.g. sole trader) vs a “one-person” SRO. As the tax and tax system in Slovakia is relatively complex, we have abstracted from some elements with less significant impact in order to make the calculator user-friendly and practical.

Other aspects (e.g. other income, legal liability, social security benefits) also influence the choice for a better legal form of business. If you have questions, we will be happy to answer them.

These forms are for an indicative comparison of the net income for 2025 of a self-employed entrepreneur (e.g. sole trader) vs a “one-person” SRO. As the tax and taxation system in Slovakia is relatively complex, we have abstracted from some elements with less significant impact in order to make the calculator user-friendly and practical.

Other aspects (e.g. other income, legal liability, social security benefits) also influence the choice for a better legal form of business. If you have questions, we will be happy to answer them.

In 2026, the amount of the applicable subsistence minimum, which is the basis for a number of tax and levy calculations and indicators, such as the non-taxable parts of the tax base, will change. For 2026, the subsistence minimum is based on EUR 284.13 per month, which represents a slight increase compared to the previous year.

Calculations of taxable earnings and tax “thresholds” are also based on the average wage in the national economy. For 2026, the average wage two years back, so for 2024, which amounted to EUR 1 524, is decisive.

The dividend tax rate is 7%. Care should be taken as to what period the dividends relate to and the correct tax rate should be applied as the tax rate is 10% during 2024.

Legal entities, such as limited companies, will apply four rates for 2026:

CSOs have an advantage over individuals who are not CSOs in the form of a reduced tax rate of 15%. For the self-employed, the following tax rates apply:

Employees or executives with earned income will pay the following in 2026:

Self-employed persons will pay contributions:

The minimum taxable amount for contributions of self-employed persons increases to EUR 914.40 from January 2026. The maximum assessment base will reach EUR 16,764 for most social levies. Health levies do not have a cap.

The non-taxable part of the tax base (NČZD) per taxpayer increases to EUR 5,966.73 (21 times the applicable minimum subsistence level) in 2026, while its amount decreases with a higher tax base. If the tax base of a sole trader is equal to or higher than EUR 43,983.32 per year, the amount of the non-taxable part of the tax base is EUR 0.00.

A spouse may be eligible for NHT in the amount of:

Taxpayers can still claim a deduction for supplementary pension savings (Pillar III) of up to EUR 180 per year.

Fixed tax bonus amounts:

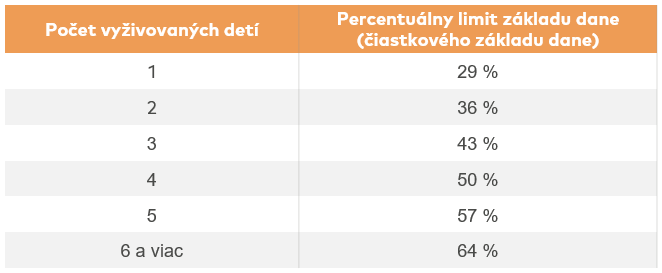

However, the amount of the tax bonus may be up to a maximum of the product of the relevant percentage and the taxpayer’s tax base. The individual percentages are as follows:

Taxpayers can also benefit from a 50% tax bonus on mortgage interest paid, with a maximum tax bonus of €1,200 per year for contracts signed after 1 January 2024.

Lump-sum expenditure remains at 60% of income in 2026, capped at €20,000 per year.

There are rules for the payment of advance income tax for both corporations and individuals:

In the case of an individual or legal entity seeking to capitalise its assets through capital market instruments, the tax legislation is complex and it is not possible to clearly determine the tax liability without further analysis. Examples might be the most advantageous foreign currency to euro conversion for an individual or the application of double taxation treaty provisions. In the case of legal entities and some self-employed persons, proper accounting with an emphasis on the tax implications of individual transactions is necessary. More about investment portfolios