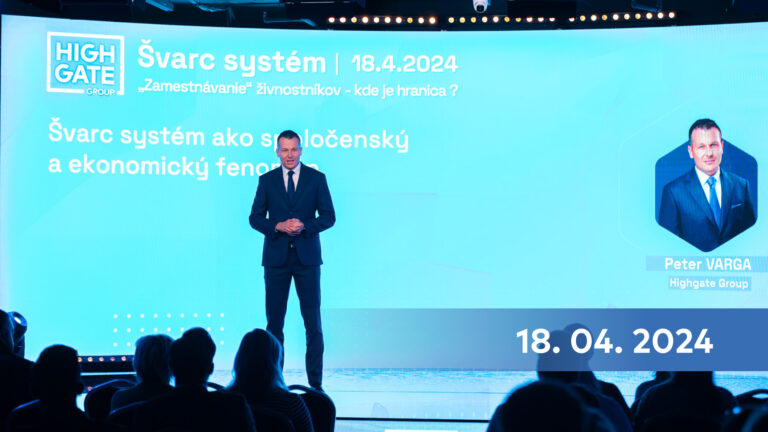

Peter Varga is the founder and CEO of Highgate Group, a Slovak consulting firm providing legal, tax, accounting, and other business advisory services. Peter Varga specializes in tax consulting, financial regulation consulting, and corporate law. Among specific topics, he has recently devoted considerable attention to advising investment funds, issues related to the so-called “Švarc system,” various tax and legal structures and arrangements, advises on M&A, private equity, and venture capital investments, and represents clients in connection with tax audits and proceedings before the National Bank of Slovakia. Peter is the chair of the Legal & Tax Committee of SLOVCA, serves as an advisor on various public and legislative initiatives, lectures regularly, and is active as an author. Peter graduated from the Faculty of Law at Comenius University, the University of Economics in Bratislava, and also spent some time at the University of Regensburg and the London School of Economics.

in

Ondřej Trubač is a co-founder and partner at the law firm Bříza & Trubač, where he specializes primarily in complex tax law issues, particularly in representing clients in disputes with tax authorities during tax proceedings as well as before administrative and constitutional courts. He also focuses on criminal tax law, related issues of effective repentance, and the criminal liability of legal entities. He graduated from the Faculty of Law at Charles University (Mgr., JUDr., Ph.D.) and earned an LL.M. from Christian-Albrechts-Universität zu Kiel. He serves as Vice President of the Czech Bar Association and Chair of the Section for Bar Law. He is a co-author of commentaries on the Financial Administration Act, the Act on the Proving of the Origin of Property, and the Civil Code, as well as the successful publication *Defense Against Tax Audits*. He regularly lectures at universities and for the legal profession, publishes in professional journals, and co-organizes conferences (e.g., Criminal Tax Law, Tax Compliance). He is repeatedly ranked in the prestigious The Legal 500 (Leading Partner) and Chambers Europe rankings.

inMiesto: Bratislava

Speaker: Peter Varga

Speaker: Peter Varga

Speaker: Ondřej Trubač

{kind=link}

{kind=link}